SARL de Famille and LMNP: all you need to know about this combination

The combination of a family limited liability company and Non-Professional Furnished Renter status (LMNP) represents an increasingly popular real estate investment strategy. Indeed, it combines the flexibility of a limited liability company dedicated exclusively to members of the same family with the attractive tax advantages of LMNP or LMP status (depending on the turnover generated). This synergy allows real estate investors, whether beginners or experienced, to benefit from a fiscal optimization significant, while facilitating the management and transmission of real estate assets.

The family limited liability company: structure and operation

The SARL de Famille, a specific legal system within French law, is distinguished by its flexible structure and adapted to family real estate investment projects, in particular in non-professional furnished rentals (LMNP). This type of limited liability company offers a beneficial framework for the management and fiscal optimization of real estate assets, thus combining economic performance and family cohesion.

Composition and characteristics of a family SARL

- Composition: the SARL de Famille consists exclusively of members of the same family (spouses, PACS partners, ascendants, descendants, and collaterals up to the 2nd degree).

- Social capital: free, social capital can be variable and adapted to the needs of the company and partners, thus promoting accessibility to all investor profiles.

- Number of partners: 2 partners at least, with no maximum limit.

Benefits of fiscal transparency for family members

- Direct taxation: the profits made by SARL de Famille are taxed directly in the hands of the partners, in proportion to their shares, which makes it possible to benefit from allowances for duration of ownership and personal tax brackets.

- Tax optimization: the possibility of choosing income tax (IR) instead of corporate tax (IS) (provided that the activity is either industrial, commercial, artisanal or agricultural) opens the door to advantageous tax management, in particular by exploiting tax niches relating to the LMNP.

- Social security for the self-employed: Majority managers fall under the self-employed regime, which can represent an advantage in terms of social security contributions.

Management and decision-making within the SARL de Famille

- Management flexibility: the structure of the SARL de Famille allows a clear distribution of roles and responsibilities, facilitating decision-making and internal organization.

- Decision making: Important decisions (modification of the articles of association, transfer of shares, approval of accounts) require the agreement of the partners, in accordance with the procedures defined in the articles of association.

- Transmission and continuity: The SARL de Famille facilitates the transmission of real estate assets to the following generations, while ensuring the continuity of the rental activity.

You hesitate between different regimes, take an expert call for a simulation

The LMNP tax regime in a family SARL

The combination of a Family SARL with the status of Non-Professional Furnished Lessor (LMNP) creates a powerful real estate investment structure, allowing optimized and flexible tax management.

Real estate amortization in LMNP within a family limited liability company

Depreciation is one of the main attractions of the LMNP regime, offering significant tax optimization:

- Allows you to spread the cost of acquiring the property (excluding land) over its duration of use.

- Reduces the tax base, thus making it possible to reduce taxes on the rental income generated.

- Promotes the constitution of real estate assets by optimizing the annual tax burden.

Treatment of real estate capital gains in family limited liability companies

The sale of furnished real estate owned via a family limited liability company under the LMNP regime is accompanied by specific rules concerning capital gains:

- Taxation of capital gains : subject to the regime of capital gains for individuals, with an allowance for length of detention, offering total exemption after 22 years of detention for income tax and 30 years for social security contributions.

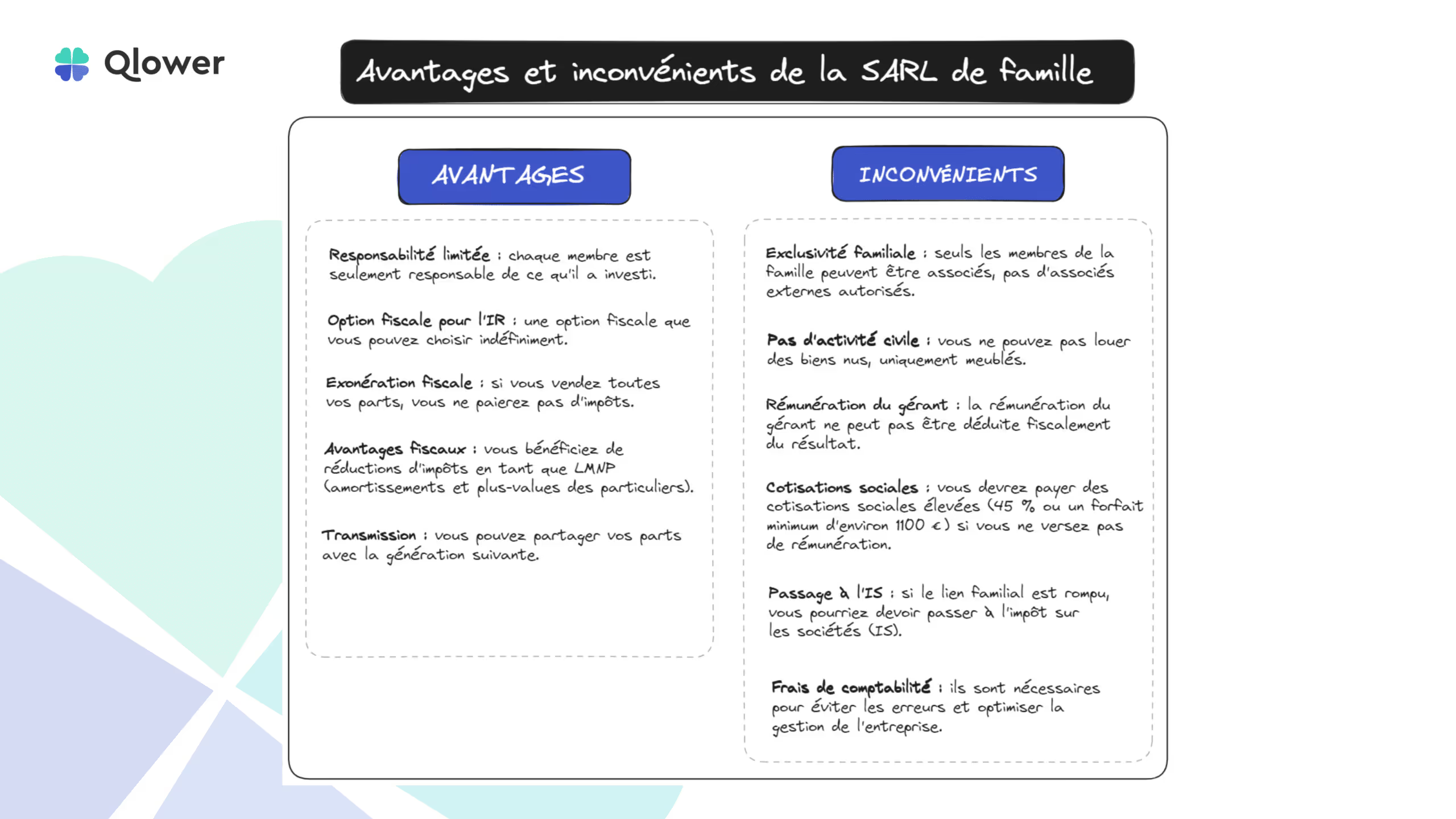

Advantages of a family limited liability company for furnished rentals

The SARL de Famille, when combined with the status of Non-Professional Furnished Renter (LMNP) or Professional (LMP), offers a series of significant advantages for real estate investors, particularly in terms of tax optimization, asset transfer management, and family wealth protection.

Tax optimization and flexibility of the LMNP regime

The SARL de Famille en LMNP is distinguished by its ability to offer remarkable fiscal optimization, accompanied by great flexibility in the management of real estate investments:

- Tax transparency allows the profits of the SARL de Famille to be taxed on behalf of the partners according to their personal tax bracket, which can be more advantageous than corporate tax rates.

- Partners can decide how to distribute profits in order to optimize the family's overall tax burden.

Easy transfer of assets and succession

One of the main advantages of a SARL de Famille en LMNP lies in the simplification of asset transmission and succession:

- The shares in SARL de Famille can be given to family members, thus allowing a gradual transmission of real estate assets, often benefiting from attractive tax allowances.

- The structure allows for more strategic and less expensive estate planning, compared to directly owning real estate.

- The SARL de Famille facilitates the continuity of the management of rental real estate in the event of the death of one of the partners, thus avoiding the complications associated with joint ownership.

Protection of family assets and separation of assets

The creation of a family SARL in LMNP also makes it possible to protect family assets and to ensure a clear separation of assets:

- The partners of SARL de Famille are only responsible for the amount of their contributions, thus protecting their personal assets in the event of debts or financial difficulties of the company.

- The distinction between the personal assets of the partners and that of the company facilitates the management of assets and offers protection in the event of disputes or claims from creditors.

Creation and management of a family SARL in LMNP

The creation and management of a family limited liability company in LMNP is a structured process, requiring particular attention to legal, fiscal and administrative details. This structure offers great flexibility and numerous tax advantages, but it also requires compliance with certain formalities and obligations.

Stages and formalities for creating a family SARL

The establishment of a family SARL in LMNP follows a regulated process:

- Drafting the statutes : the articles of association must be carefully written to frame the operating rules of the SARL de Famille, including the company name, information on the founders, the identity of the company, the share capital and the distribution of shares between the partners.

- Deposit of share capital : the share capital must be deposited in a bank to obtain a certificate of deposit of funds.

- Notice in a legal notice holder : this process, carried out online at a cost of around 200 euros, makes it possible to make the event public and enforceable, with a publication certificate issued by the medium of legal announcements.

- Form M0: is a document that the entrepreneur must complete to declare the constitution of his company. This process leads to the registration of the SARL, whether it is the Trade and Companies Register (RCS) or the Trade Directory (RM).

- RCS registration : the company must be registered in the Trade and Companies Register, which involves the submission of a file including the signed articles of association, the certificate of deposit of funds, a certificate of non-conviction for the manager (s), the form M0, and a legal announcement of constitution.

Accounting management and reporting requirements

Once the SARL de Famille is created, accounting management and reporting obligations must be meticulously followed:

- The SARL de Famille en LMNP must keep complete accounts, including the entry of current transactions, the management of depreciation, and the preparation of annual accounts.

- The company must make several declarations, including the annual income statement and the VAT returns if applicable (CA3 or CA12).

- The various declarations and payments (taxes, social security contributions, etc.) must be made on time to avoid penalties.

Tips for effective and compliant management

To ensure optimal management of your LMNP family limited liability company, here are some key tips:

- Support from professionals (LMNP experts, lawyers specialized in real estate law) can be invaluable in understanding legal and fiscal complexities.

- Conduct regular tax reviews to optimize the tax burden and take full advantage of the benefits of the LMNP regime.

- Maintain regular and transparent communication within the family to make management decisions in a consensual manner.

Are you hesitating between different regimes, take an expert call?

Disadvantages and limitations of family limited liability companies in LMNP

Although a family limited liability company in LMNP has many advantages, it is also important to understand its disadvantages and limitations for strategic real estate investment management.

Administrative and accounting complexities

Managing a family limited liability company in LMNP can be complex due to administrative and accounting obligations:

- The need to maintain detailed accounting in accordance with accounting standards, including depreciation and deduction of expenses, represents a significant workload and cost.

- The multiple tax and social declarations required can be a source of confusion and increase the risk of errors or omissions.

- The effective management of a family limited liability company in LMNP requires staying informed of legislative and regulatory developments, which requires time and expertise.

Limitations related to the tax regime and the statutes

Certain aspects of the tax regime and the statutes of a SARL de Famille may also impose limitations:

- Once the choice between the micro-BIC regime and the real regime has been made, it can be difficult to change the regime due to legal and fiscal constraints.

- The articles of association should clearly define the rules for distributing profits, which can limit flexibility in the event of changes in the needs or goals of partners.

- In some cases, renting to family members may be restrictive or subject to specific conditions in order to benefit from the LMNP tax benefits.

Limits linked to the €23,000 threshold

As far as the LMNP family limited liability company is concerned, social security contributions are not payable.

Only if the threshold of €23,000 was exceeded would the activity be automatically requalified as an LMP, i.e. a professional furnished rental company. Therefore, the company should pay social security contributions.

However, a family SARL in LMNP must pay the social security contributions associated with the function of manager. Non-managing partners, for their part, are not subject to any social security contributions.

Considerations about family events (divorce, death)

Family events can have a significant impact on the management and sustainability of the SARL de Famille:

- Divorce : the separation or divorce of partners can cause complications in the management of the SARL, affecting the distribution of shares and decision-making.

- Death of a partner : although the SARL de Famille facilitates the transmission of assets, the death of a partner requires a reorganization of the company and can pose challenges in terms of succession and distribution of shares.

- Conflict Management : Disputes between family members can affect decision-making and the functioning of the SARL, requiring effective conflict resolution mechanisms.

If the family relationship is broken, the family SARL structure is forced to switch to corporate tax (IS).

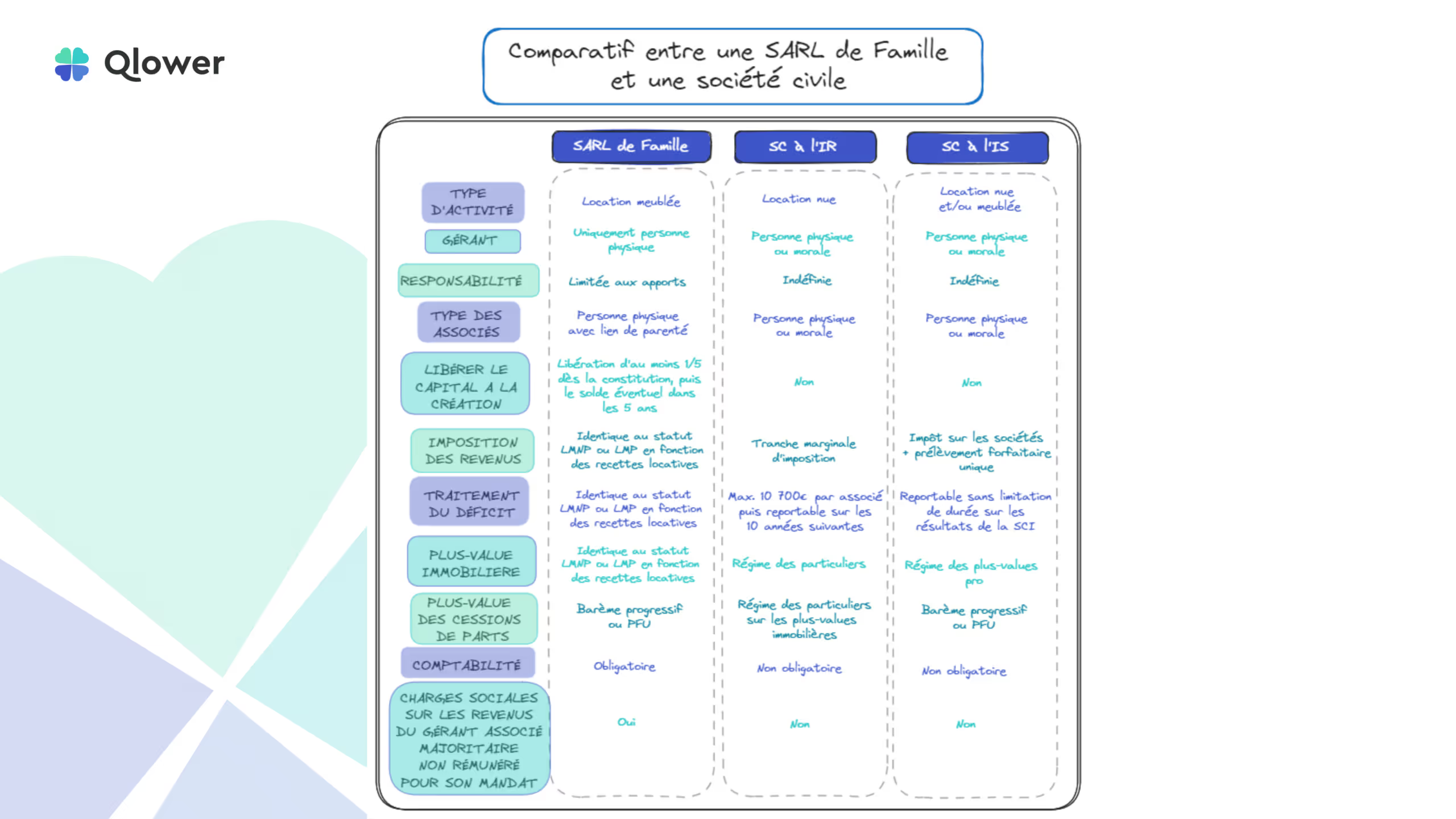

Family SARL vs. other legal structures in LMNP

Investing in a Non-Professional Furnished Rental Company (LMNP) can also find other alternatives with different legal structures, each with its own specificities, advantages, and disadvantages. Family limited liability companies, Société Civile Immobilière (SCI), and sole proprietorships represent three popular options.

Comparison with SCI and sole proprietorships

Family SARL, SCI and sole proprietorships differ mainly in their tax regime, their flexibility in terms of management, and their ability to meet the specific objectives of investors:

Family SARL:

- Preferred structure for family management.

- Enables fiscal optimization thanks to fiscal transparency.

- Offers a limitation of liability to the contributions of partners.

SHERE:

- Oriented to the management and ownership of unfurnished rental real estate.

- Income tax or corporate tax (corporate tax) if option selected.

- Does not allow LMNP status for its associates.

Sole proprietorship:

- Adapted for management in your own name.

- Simplicity of implementation and low management costs.

- Unlimited liability for personal assets.

Relative advantages and disadvantages of each structure

Each legal structure has specific advantages and disadvantages to consider:

Family SARL:

- Benefits :

- Protection of the personal assets of partners.

- Adaptation to the LMNP regime, allowing depreciation and tax optimization benefits.

- Shared management between family members.

- Disadvantages :

- Higher administrative complexity.

- Annual creation and management costs.

SCI :

- Benefits :

- Simplicity of transmission of real estate assets.

- Clear separation of real estate assets from personal assets.

- Benefits :

- Disadvantages:

- Non-eligibility for LMNP status, limiting the tax advantages associated with depreciation under the IR and the absence of an allowance for the duration of detention under the IS. ”

- Responsibility of partners in proportion to their shares in certain cases.

Sole proprietorship:

- Benefits :

- Great administrative simplicity and freedom of management.

- Direct application of the LMNP regime for tax optimization.

- Disadvantages :

- Unlimited personal liability, exposing personal assets in case of debts.

- Less suitable for long-term asset management with transmission objectives.